This article was published as a part of the Data Science Blogathon.

Cryptocurrencies are digital tokens that can easily replace traditional currency in the future. Easy access is the reason they are becoming so popular so fast. Almost anyone can own these coins and are accepted as payment just like traditional currency.

The blockchain technology on which most of these tokens are based, and their decentralized systems can have many more implementations in creating more safe and secure organizational environments in the future. In theory, it can change how economies and industries work and can almost effectively eliminate inefficiency and human error.

Like I said we are on the verge of something new and exciting, and getting on the ground floor of this change can benefit us and our successors in ways unimaginable. But how about we start this exciting crypto stuff with some good old data science analysis?

Dataset

You can find the dataset we will use here: Kaggle: Cryptocurrency

Let’s start with some EDA.

Exploratory Data Analysis

Python Code:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from datetime import datetime, timedelta

import warnings

warnings.filterwarnings('ignore')

import matplotlib.dates as mdates

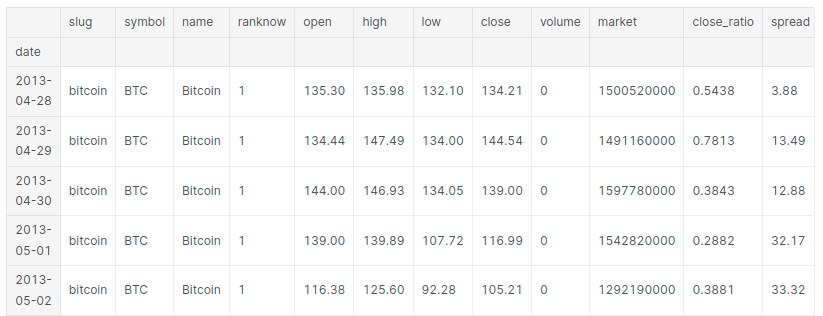

df = pd.read_csv('crypto-markets.csv')

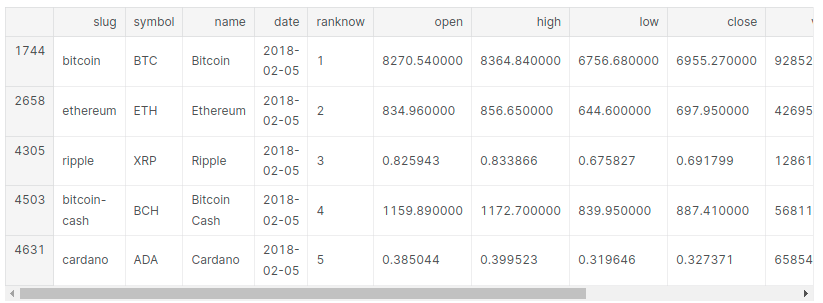

print(df.head())Open The price of the coin at the beginning of the trading day.

High: The highest price of the coin on a trading day.

Low: The lowest price of the coin on a trading day.

Close: The last price of the coin before the trading day ends.

# Transforming date to date object df['date'] = pd.to_datetime(df['date'], format='%Y-%m-%d')

# Getting a dataframe containing only the latest date's data for each currency

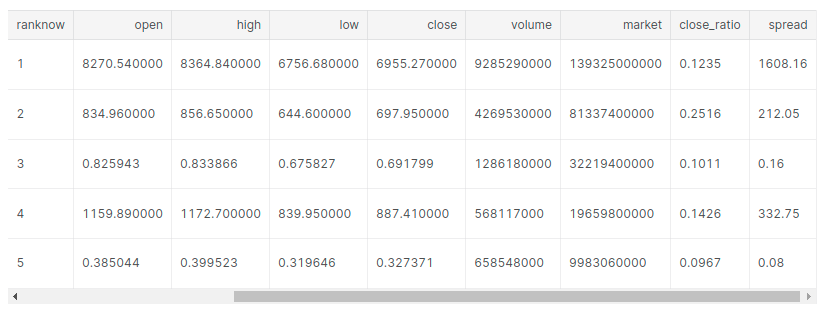

print("Latest crypto data")

latest_df = df[df['date'] == max(df['date'])]

latest_df.head()

print("Number of cryptocurrencies listed: ")

latest_df['symbol'].nunique()

> Number of cryptocurrencies listed: 1461

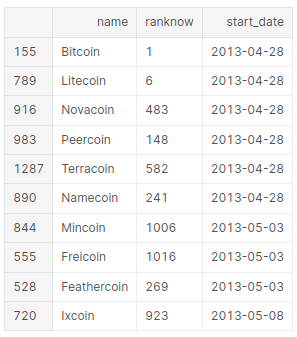

Old and new tokens

# starting dates for all currencies

start_df = pd.DataFrame({'start_date' : df.groupby( [ "name", "ranknow"] )['date'].min()}).reset_index()

# List the oldest ones

print("Oldest Cryptocurrencies")

start_df.sort_values(['start_date']).head(x)

Oldest Cryptocurrencies

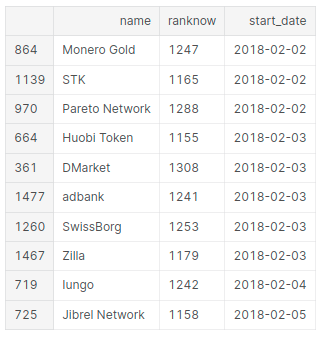

# List of the new ones

print("New Cryptocurrencies")

start_df.sort_values(['start_date']).tail(x)

New Cryptocurrencies

Rank

latest_df[latest_df['ranknow'] <= x].groupby('ranknow').name.unique()

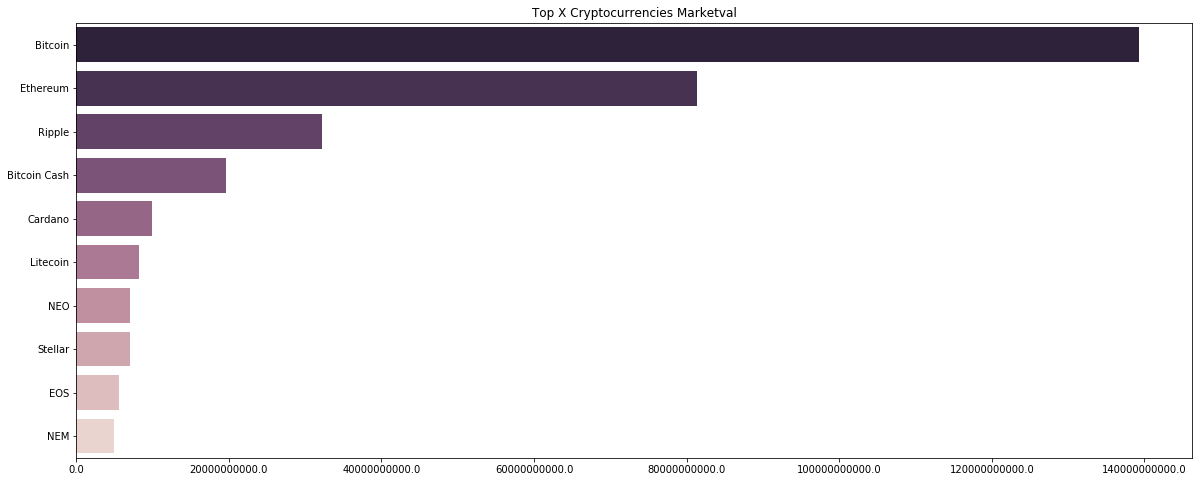

Market capitalization

We can calculate this value by multiplying the current price of the token with the total amount circulating in the market.

# Plotting the top X currencies according to market valuation

name = latest_df['name'].unique()

currency = []

marketval = []

x_currencies = name[:x]

for i, cn in enumerate(x_currencies):

filtered = latest_df[(latest_df['name']==str(cn))]

currency.append(str(cn))

marketval.append(filtered['market'].values[0])

f, ax = plt.subplots(figsize=(20, 8))

g = sns.barplot( y = currency, x = marketval, palette=sns.cubehelix_palette(x, reverse=True))

plt.title("Top X Cryptocurrencies Marketval")

ax.set_xticklabels(ax.get_xticks())

fig=plt.gcf()

plt.show()

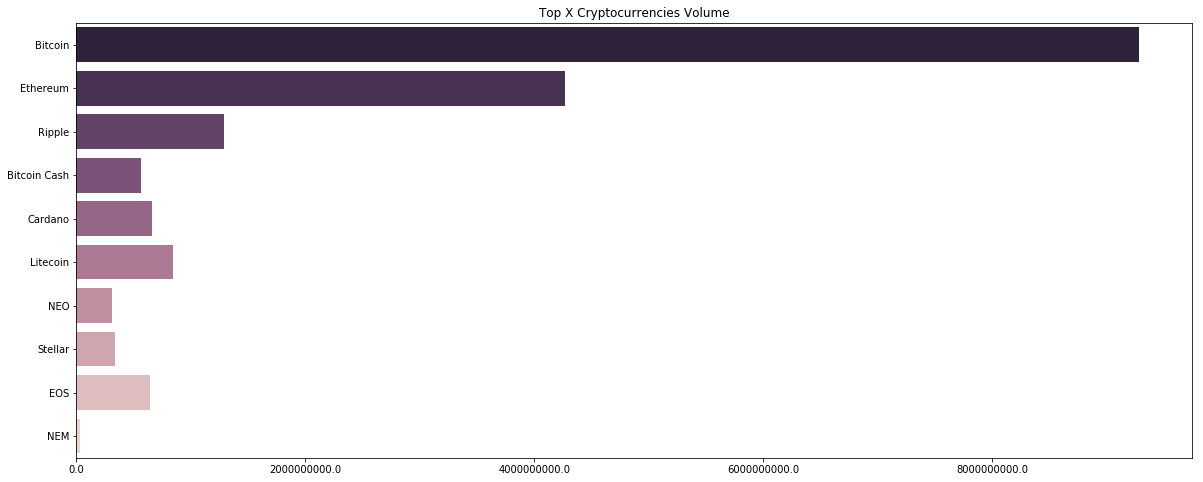

Volume

In simple words, Volume is the amount of a token traded in a specific time interval.

# Plotting the top X currencies by volume

latest_df

currency = []

volume = []

x_currencies = name[:x]

for i, cn in enumerate(x_currencies):

filtered = latest_df[(latest_df['name']==str(cn))]

currency.append(str(cn))

volume.append(filtered['volume'].values[0])

f, ax = plt.subplots(figsize=(20, 8))

g = sns.barplot( y = currency, x = volume, palette=sns.cubehelix_palette(x, reverse=True))

plt.title("Top X Cryptocurrencies Volume")

ax.set_xticklabels(ax.get_xticks())

fig=plt.gcf()

plt.show()

The crypto market much like the stock market depends a lot on the trader’s sentiments. The buyers are the ones who increase the price and the sellers are the ones who drive the price low. An increase in price but a decrease in volume traded shows a lack of interest, and thus can end up in a potential reversal. I know it’s counterintuitive, but that’s how financial markets all over the world works.

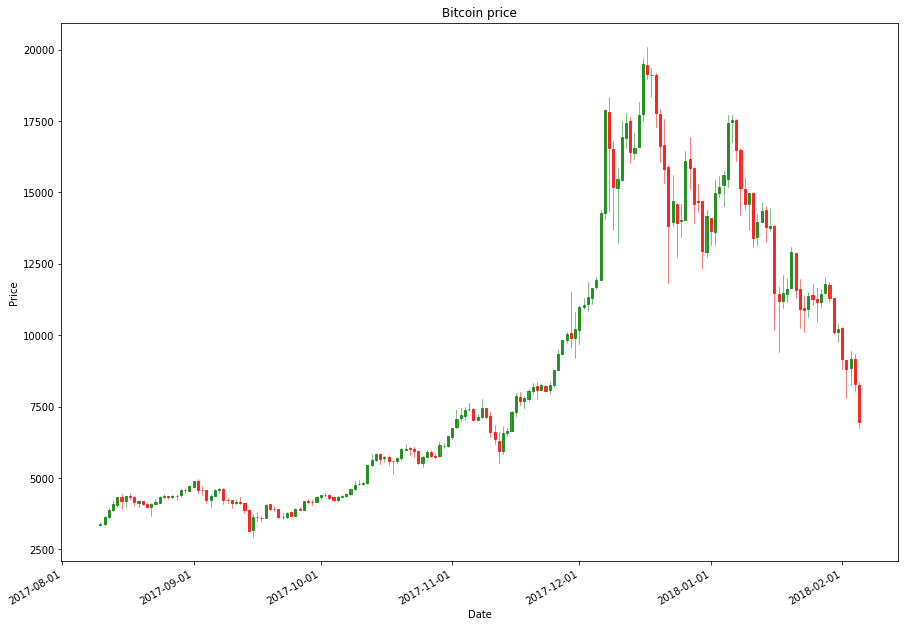

In this next section, we will use candlestick charts, which is the most popular chart-type used by traders, along with indicators like moving average to see if we can track some changes in volumes and uptrends and downtrends in the crypto market.

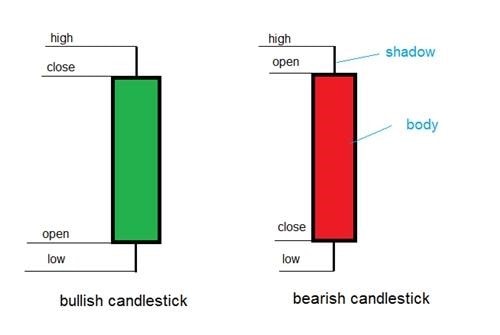

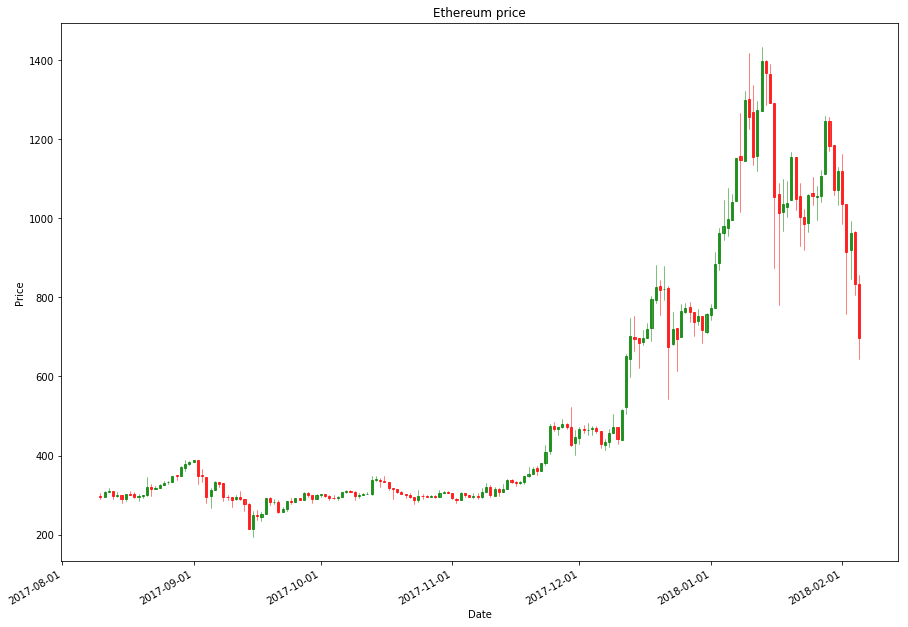

Japanese Candlestick

Image Source: Japanese Candlesticks: Find reliable signals

There are 2 types of candles in a Japanese candlestick pattern, a green and a red. The green one signifies the price increased in the given time interval and the red one vice versa. The rectangular part of a candlestick is its body. In a green candle, the bottom end is the opening price and the upper one is the closing price. The 2 wicks out of the rectangle from both sides are called shadows, which signify the high and low price for that timeframe.

# Candlestick chart for Bitcoin

rank = 1

months = 6

name = df[df.ranknow == rank].iloc[-1]['name']

filtered_df = df[(df['ranknow'] == rank) & (df['date'] > (max(df['date']) - timedelta(days=30*months)))]

OHLCfiltered_df = filtered_df[['date','open','high','low','close']]

OHLCfiltered_df['date'] = mdates.date2num(OHLCfiltered_df['date'].dt.date)

f,ax=plt.subplots(figsize=(15,11))

ax.xaxis_date()

candlestick_ohlc(ax, OHLCfiltered_df.values, width=0.5, colorup='g', colordown='r',alpha=0.75)

plt.xlabel("Date")

ax.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d'))

plt.gcf().autofmt_xdate()

plt.title(name + " price")

plt.ylabel("Price")

plt.show()

# Candlestick chart for Etherium

rank = 2

months = 6

name = df[df.ranknow == rank].iloc[-1]['name']

filtered_df = df[(df['ranknow'] == rank) & (df['date'] > (max(df['date']) - timedelta(days=30*months)))]

OHLCfiltered_df = filtered_df[['date','open','high','low','close']]

OHLCfiltered_df['date'] = mdates.date2num(OHLCfiltered_df['date'].dt.date)

f,ax=plt.subplots(figsize=(15,11))

ax.xaxis_date()

candlestick_ohlc(ax, OHLCfiltered_df.values, width=0.5, colorup='g', colordown='r',alpha=0.75)

plt.xlabel("Date")

ax.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d'))

plt.gcf().autofmt_xdate()

plt.title(name + " price")

plt.ylabel("Price")

plt.show()

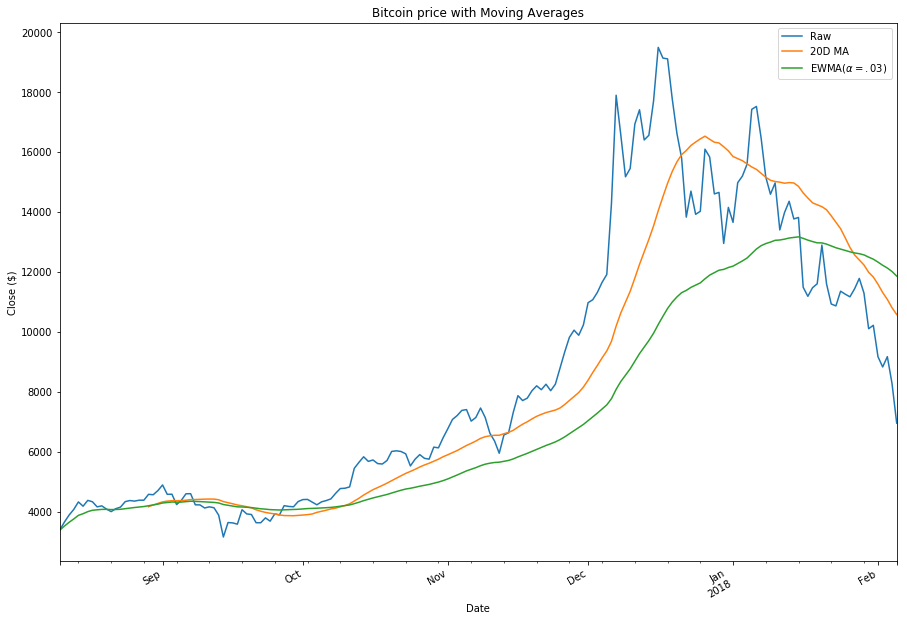

Moving average

We can use SMA(simple moving average) which is a very popular indicator in stock trading, to analyze the trends in the market.

# Moving average chart for Bitcoin

rank = 1

months = 6

name = df[df.ranknow == rank].iloc[-1]['name']

filtered_df = df[(df['ranknow'] == rank) & (df['date'] > (max(df['date']) - timedelta(days=30*months)))]

filtered_df.set_index('date', inplace=True)

f, ax = plt.subplots(figsize=(15,11))

filtered_df.close.plot(label='Raw', ax=ax)

filtered_df.close.rolling(20).mean().plot(label='20D MA', ax=ax)

filtered_df.close.ewm(alpha=0.03).mean().plot(label='EWMA($\alpha=.03$)', ax=ax)

plt.title(name + " price with Moving Averages")

plt.legend()

plt.xlabel("Date")

plt.gcf().autofmt_xdate()

plt.ylabel("Close ($)")

plt.show()

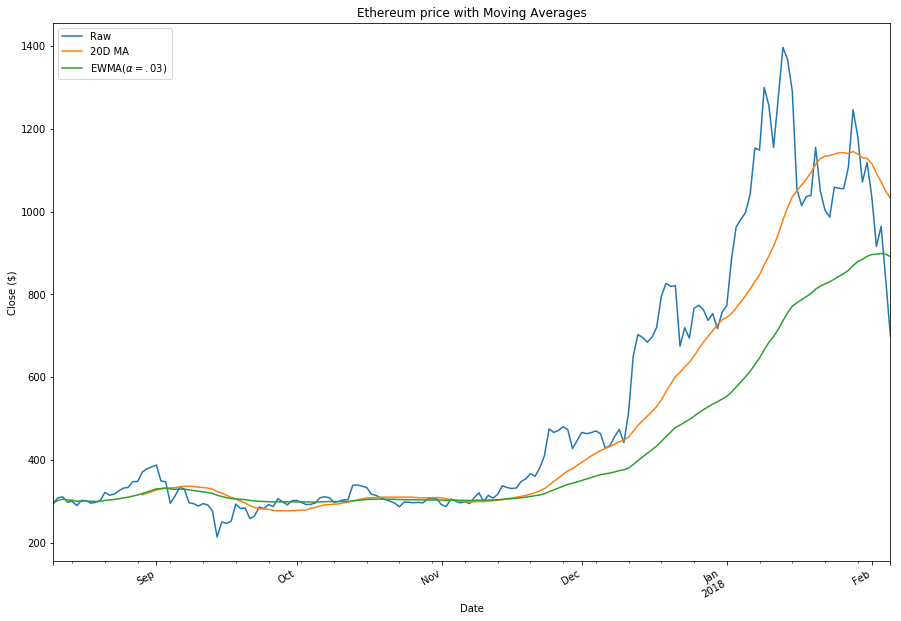

# Moving average chart for Etherium

rank = 2

months = 6

name = df[df.ranknow == rank].iloc[-1]['name']

filtered_df = df[(df['ranknow'] == rank) & (df['date'] > (max(df['date']) - timedelta(days=30*months)))]

filtered_df.set_index('date', inplace=True)

f, ax = plt.subplots(figsize=(15,11))

filtered_df.close.plot(label='Raw', ax=ax)

filtered_df.close.rolling(20).mean().plot(label='20D MA', ax=ax)

filtered_df.close.ewm(alpha=0.03).mean().plot(label='EWMA($\alpha=.03$)', ax=ax)

plt.title(name + " price with Moving Averages")

plt.legend()

plt.xlabel("Date")

plt.gcf().autofmt_xdate()

plt.ylabel("Close ($)")

plt.show()

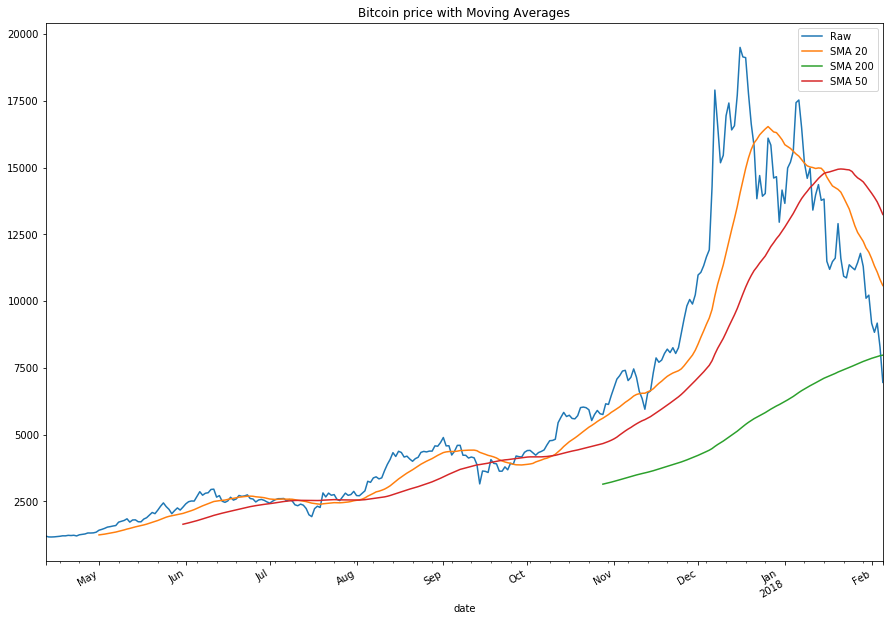

Here are a few well-known facts about using the SMA in the stock market:

- The 20 moving average (20MA) is used for the short-term analysis.

- The 50 moving average (50MA) is used for medium-term analysis.

- The 200 moving average (200MA) is used to determine the trend.

In a bullish run (uptrend) the price of the stock should be above 20 MA, and the 50 MA in between 20 MA and 200 MA. And in a bear run (downtrend), the vice versa.

Let’s see if that is the case with our top 2 cryptocurrencies: Bitcoin and Etherium.

# Moving average chart for BTC

rank = 1

months = 10

name = df[df.ranknow == rank].iloc[-1]['name']

filtered_df = df[(df['ranknow'] == rank) & (df['date'] > (max(df['date']) - timedelta(days=30*months)))]

filtered_df.set_index('date', inplace=True)

sma20 = filtered_df.close.rolling(20).mean()

sma50 = filtered_df.close.rolling(50).mean()

sma200 = filtered_df.close.rolling(200).mean()

smaplot =pd.DataFrame({'Raw': filtered_df.close, 'SMA 20': sma20, 'SMA 50': sma50, 'SMA 200': sma200})

smaplot.plot(figsize=(9,5), legend=True, title="Bitcoin price with Moving Averages")

plt.gcf().autofmt_xdate()

plt.show()

As you can see a classic uptrend in mid-November 2017. After a few crosses between the coin price and the 20 SMA, we see a clear uptrend in 2017 end. But before not so long, we see a clear trend reversal in early January, indicating the beginning of a bear run.

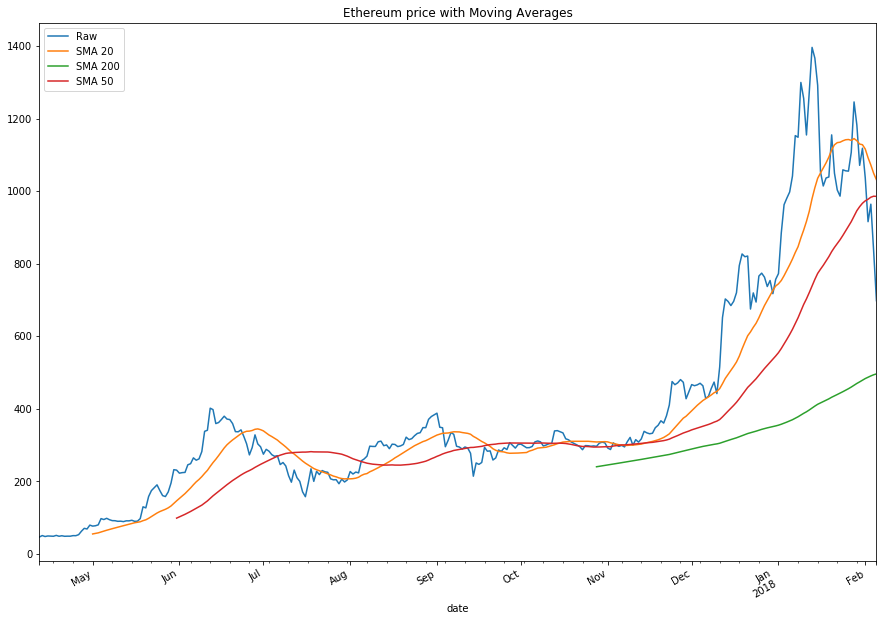

# Moving average chart for ETH

rank = 2

months = 10

name = df[df.ranknow == rank].iloc[-1]['name']

filtered_df = df[(df['ranknow'] == rank) & (df['date'] > (max(df['date']) - timedelta(days=30*months)))]

filtered_df.set_index('date', inplace=True)

# simple moving averages

sma20 = filtered_df.close.rolling(20).mean()

sma50 = filtered_df.close.rolling(50).mean()

sma200 = filtered_df.close.rolling(200).mean()

smaplot = pd.DataFrame({'Raw': filtered_df.close, 'SMA 20': sma20, 'SMA 50': sma50, 'SMA 200': sma200})

smaplot.plot(figsize=(9,5), legend=True, title="Etherium price with Moving Averages")

plt.gcf().autofmt_xdate()

plt.show()

Etherium had a similar uptrend in late 2017 but mostly had a sideways market in most of 2017. In early 2108 we can see the 20 MA starting to change directions, which can possibly result in a bear run, but as of now, there’s no clear indication.

Price Prediction using ARIMA

In this section, we will use ARIMA(AutoRegressive Integrated Moving Average) to predict the price of Bitcoin using past data and the above analysis.

Importing libraries

import pandas as pd

from pandas import DataFrame

import numpy as np

import matplotlib.pyplot as plt

plt.rcParams["figure.figsize"] = (15,7)

import seaborn as sns

from datetime import datetime, timedelta

from statsmodels.tsa.arima_model import ARIMA

from statsmodels.tsa.statespace.sarimax import SARIMAX

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.stattools import adfuller

from statsmodels.tsa.seasonal import seasonal_decompose

from scipy import stats

import statsmodels.api as sm

from itertools import product

import warnings

warnings.filterwarnings('ignore')

Importing data

dateparse = lambda dates: pd.datetime.strptime(dates, '%Y-%m-%d')

df = pd.read_csv('../input/crypto-markets.csv', parse_dates=['date'], index_col='date', date_parser=dateparse)

df.head()

df.tail()

# Extracting bitcoin data btc=df[df['symbol']=='BTC'] btc.drop(['slug', 'volume','symbol','name','ranknow','market', 'close_ratio', 'spread'],axis=1,inplace=True)

btc.head()

ARIMA Model

AutoRegressive Integrated Moving Average

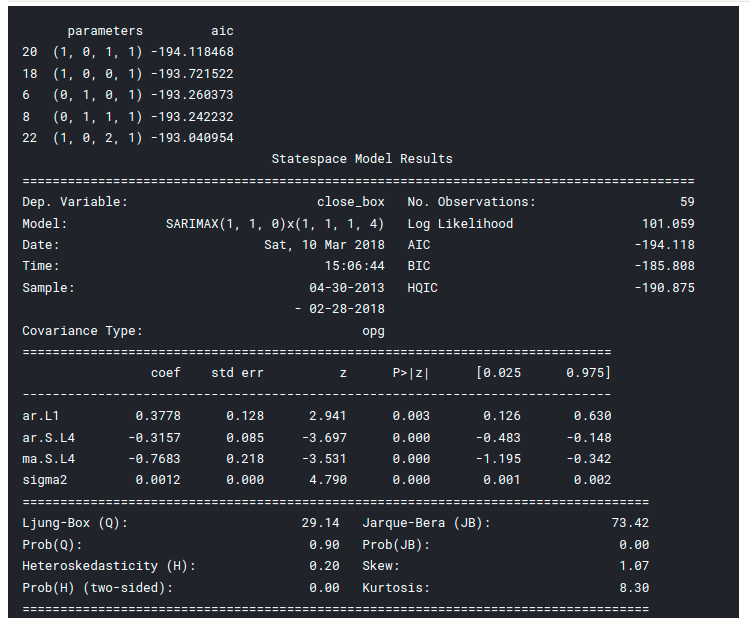

The model has 3 parameters p, d, and q accounting for seasonality, trend, and noise in the dataset. We will fit the ARIMA model using a stats model which will return something called an AIC value (Akaike Information Criterion). The AIC scales how compatible the model fits the data and the complexity of the model. A model with a lot of features that fit the data will be given a larger AIC score, than a model with the same accuracy but a lesser number of features. Thus we are looking for a model which yields a low AIC score. Let’s get started :

# Initial approximation of parameters

qs = range(0, 3)

ps = range(0, 3)

d=1

parameters = product(ps, qs)

parameters_list = list(parameters)

len(parameters_list)

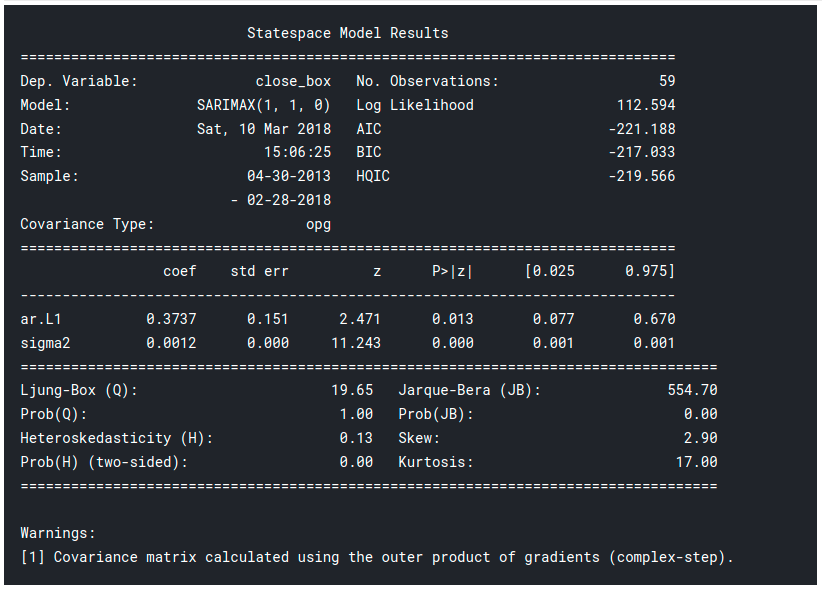

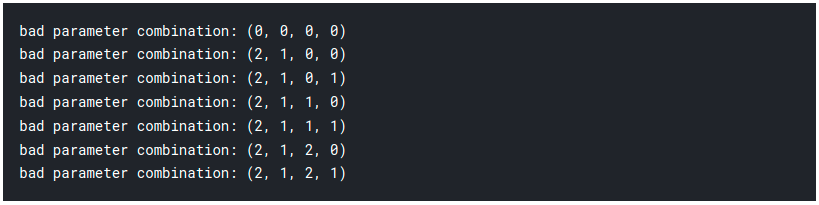

# Model Selection

results = []

best_aic = float("inf")

warnings.filterwarnings('ignore')

for param in parameters_list:

try:

model = SARIMAX(btc_month.close_box, order=(param[0], d, param[1])).fit(disp=-1)

except ValueError:

print('bad parameter combination:', param)

continue

aic = model.aic

if aic < best_aic:

best_model = model

best_aic = aic

best_param = param

results.append([param, model.aic])

# Best Models result_table = pd.DataFrame(results) result_table.columns = ['parameters', 'aic'] print(result_table.sort_values(by = 'aic', ascending=True).head())

print(best_model.summary())

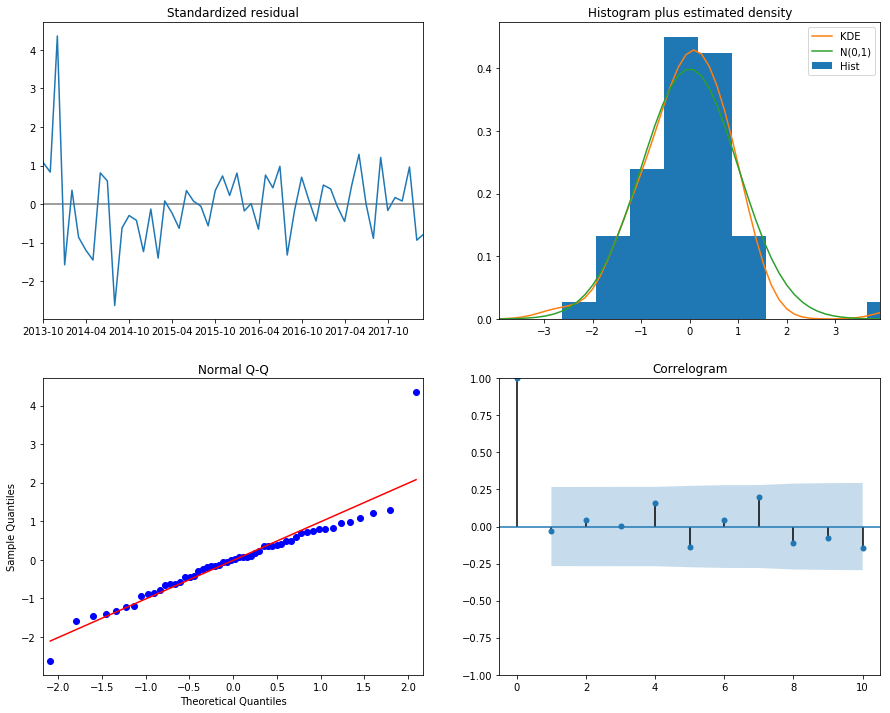

Results

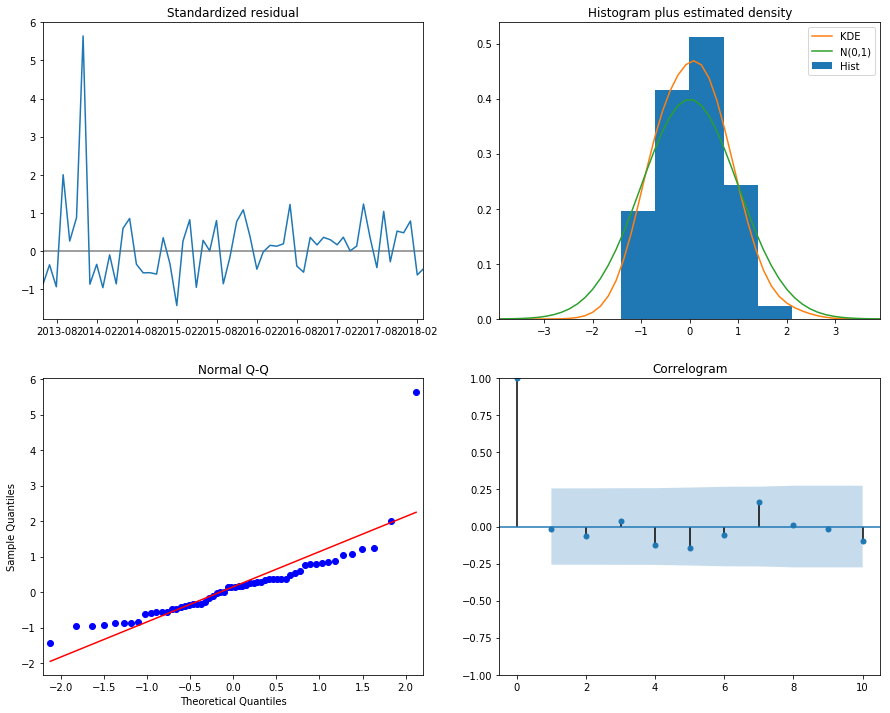

print("Dickey–Fuller test:: p=%f" % adfuller(best_model.resid[13:])[1])

best_model.plot_diagnostics(figsize=(15, 12)) plt.show()

Now it’s time for some prediction!

Prediction

btc_pred = btc_month[['close']] date_list = [datetime(2018,6,31), datetime(2018,5,30), datetime(2018,3,31), datetime(2018,4,30)] future = pd.DataFrame(index=date_list, columns= btc_month.columns) btc_pred = pd.concat([btc_month_pred, future]) btc_pred['forecast'] = invboxcox(best_model.predict(start=datetime(2014,1,31),end=datetime(2018,6,30)),lmbda)

plt.figure(figsize=(15,7))

btc_month_pred.close.plot()

btc_month_pred.forecast.plot(color='r', ls='--', label='Predicted Close')

plt.legend()

plt.title('Bitcoin monthly forecast')

plt.ylabel('USD')

plt.show()

SARIMAX Model

It stands for Seasonal ARIMA with eXogenous regressors model.

The bitcoin data above showed some seasonality which was unexpected. Therefore we can improve our model using SARIMA.

# Initial approximation of parameters

Qs = range(0, 2)

qs = range(0, 3)

Ps = range(0, 3)

ps = range(0, 3)

D=1

d=1

parameters = product(ps, qs, Ps, Qs)

parameters_list = list(parameters)

len(parameters_list)

# Model Selection

results = []

best_aic = float("inf")

warnings.filterwarnings('ignore')

for param in parameters_list:

try:

model = SARIMAX(btc_month.close_box, order=(param[0], d, param[1]), seasonal_order=(param[2], D, param[3], 4)).fit(disp=-1)

except ValueError:

print('bad parameter combination:', param)

continue

aic = model.aic

if aic < best_aic:

best_model = model

best_aic = aic

best_param = param

results.append([param, model.aic])

# Best Models result_table = pd.DataFrame(results) result_table.columns = ['parameters', 'aic'] print(result_table.sort_values(by = 'aic', ascending=True).head()) print(best_model.summary())

Results

print("Dickey–Fuller test:: p=%f" % adfuller(best_model.resid[13:])[1])

best_model.plot_diagnostics(figsize=(15, 12)) plt.show()

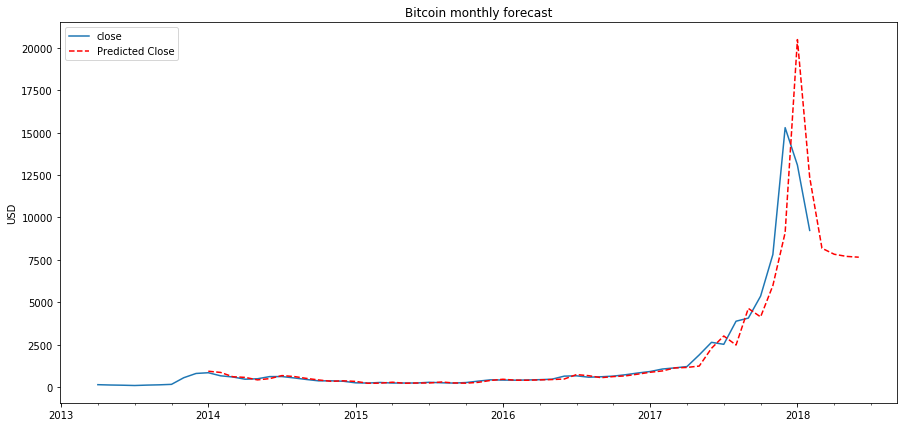

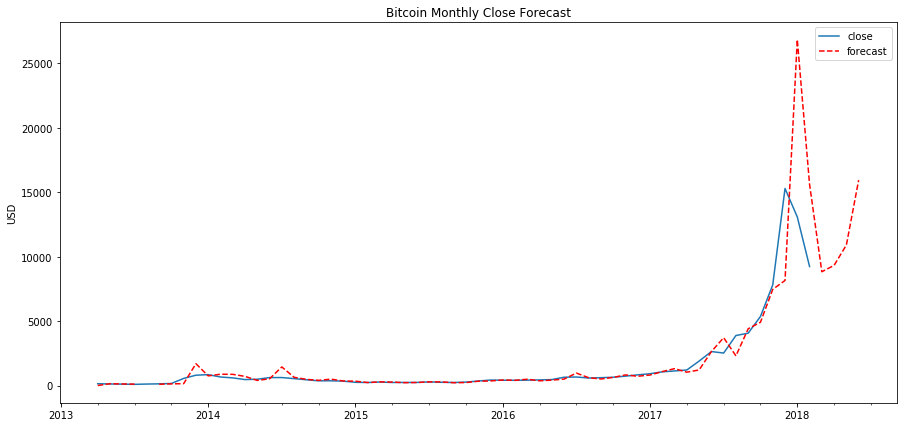

Prediction of the ARIMA Model

btc_month2 = btc_month[['close']]

date_list = [datetime(2018,6,31),datetime(2018,5,30),datetime(2018,3,31),datetime(2018,4,30)]

future = pd.DataFrame(index=date_list, columns= btc_month.columns)

btc_month2 = pd.concat([btc_month2, future])

btc_month2['forecast'] = invboxcox(best_model.predict(start=0, end=75), lmbda)

plt.figure(figsize=(15,7))

btc_month2.close.plot()

btc_month2.forecast.plot(color='r', ls='--', label='forecast')

plt.legend()

plt.title('Bitcoin Monthly Close Forecast')

plt.ylabel('USD')

plt.savefig('bitcoin_monthly_forecast.png')

plt.show()

Validation

Now we will calculate how accurate our prediction is using RMSE (root mean square error). Let’s calculate the RMSE for 2015 through 2017:

y_forecasted = btc_month2.forecast

y_truth = btc_month2['2015-01-01':'2017-01-01'].close

# Compute the root mean square error

rmse = np.sqrt(((y_forecasted - y_truth) ** 2).mean())

print('Mean Squared Error: {}'.format(round(rmse, 2)))

End Notes

Thank you for taking out the time to read this article. If you liked my work and want to read more of it here’s the link to my Analytics Vidhya profile, be sure to check it out:

Sion | Author at Analytics Vidhya

Thanks and cheers!

I am doing my PDP in Data Science and this post is really useful in that context. ARIMA works well in a time series.

This ARIMA model looks pretty good. It might give proper Cryptocurrency Price Prediction.

Nice post, im happy about the recent rise of the crypto market and i wish it continues. By the way i enjoy the detailed post