Introduction

Developing a prediction model for loan default involves collecting historical loan data, preprocessing it by handling missing values and encoding variables, and selecting relevant features like credit scores and employment history. Machine learning algorithms such as XGBoost in Python are then trained on this data to predict default risk. Model performance is evaluated using metrics like accuracy and precision, and the model’s predictions are used to assess risk and inform decision-making, such as adjusting loan terms or rejecting high-risk applications. Overall, Python’s machine learning libraries enable the development of effective prediction models for risk assessment and lending management.

Learning Outcomes

- Gain insight into the importance of loan defaulter prediction in financial risk assessment and decision-making.

- Learn essential data preprocessing steps such as handling missing values, encoding categorical variables, and feature selection.

- Understand the application of machine learning algorithms like XGBoost and Random Forest for loan default prediction in Python.

- Learn to evaluate model performance using metrics like accuracy, precision, recall, F1-score, and AUC in binary classification tasks.

This article was published as a part of the Data Science Blogathon.

Table of contents

Types of Default

A secured debt default can happen when a borrower fails to make payments on a mortgage loan secured by property or a business loan secured by assets. Similarly, corporate bond default occurs when a company can’t meet coupon payments. Unsecured debt defaults, like credit card debt, also impact the borrower’s credit and future borrowing capacities. These scenarios are essential in financial modeling, evaluation metrics, and learning methods, including linear regression and deep learning algorithms.

Why Do People Borrow, and Why Do Lenders Exist?

Debt is a crucial resource for individuals and businesses, enabling them to afford significant investments like homes and vehicles. However, while loans offer financial opportunities, they pose significant risks.

Lending is pivotal in driving economic growth and supporting individuals and enterprises worldwide. As economies become more interconnected, the demand for capital has surged, leading to a substantial increase in retail, SME, and commercial borrowers. While this trend has boosted revenues for many financial institutions, challenges have emerged.

In recent years, loan defaults have increased noticeably, impacting lenders’ profitability and risk management strategies. This trend underscores the importance of effective loan management, supported by sophisticated techniques such as support vector machines and gradient-based models, to accurately assess loan amounts, repayment probabilities, and overall risk profiles.

Let us work with a sample dataset to see how predicting the loan default works.

The Data

Leveraging historical client behavior data is crucial for an organization aiming to predict default on consumer lending products. By analyzing past patterns, they can identify risky and low-risk consumers, enabling them to optimize their lending decisions for future clients.

Utilizing advanced techniques like boosting, they can enhance the predictive power of their models, identifying subtle patterns and signals indicative of default risk. This approach allows for the development of robust predictive models tailored to the organization’s lending context.

Moreover, thorough validation processes ensure the reliability and accuracy of these models, validating their performance on diverse datasets and ensuring their effectiveness in real-world scenarios. By continuously refining and validating their predictive models, organizations can make informed lending decisions, mitigate risks, and maximize returns.

Predictive analytics capabilities are precious in countries like China, where the lending landscape is rapidly evolving. With the growing complexity of consumer behavior and financial transactions, leveraging data-driven insights becomes indispensable for effective risk management and decision-making in the lending sector.

The data contains each customer’s demographic features and a target variable showing whether they will default on the loan.

First, we import the libraries and load the dataset.

import numpy as np # linear algebra import pandas as pd # data processing, CSV file I/O (e.g. pd.read_csv)

import matplotlib.pyplot as plt import seaborn as sns %matplotlib inline sns.set_theme(style = "darkgrid")

Now, we read the data.

data = pd.read_csv("/kaggle/input/loan-prediction-based-on-customer-behavior/Training Data.csv")

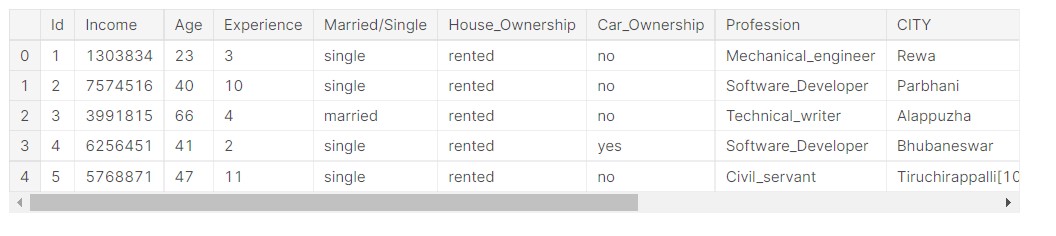

data.head()

Output:

All the dataset columns are not visible here, but I will share the link to the notebook, so please check it from there.

Understanding the Dataset

First, we start with understanding the data set and how the data is distributed.

rows, columns = data.shape

print('Rows:', rows)

print('Columns:', columns)

Output:

- Rows: 252000

- Columns: 13

So, we see that the data has 252000 rows, that is 252000 data points, and 13 columns, that is 13 features. Out of 13 features, 12 are input features, and 1 is an output feature.

Now, we check the data types and other information.

data.info()

Output:

RangeIndex: 252000 entries, 0 to 251999 Data columns (total 13 columns) # Column Non-Null Count Dtype --- ------ -------------- ----- 0 Id 252000 non-null int64 1 Income 252000 non-null int64 2 Age 252000 non-null int64 3 Experience 252000 non-null int64 4 Married/Single 252000 non-null object 5 House_Ownership 252000 non-null object 6 Car_Ownership 252000 non-null object 7 Profession 252000 non-null object 8 CITY 252000 non-null object 9 STATE 252000 non-null object 10 CURRENT_JOB_YRS 252000 non-null int64 11 CURRENT_HOUSE_YRS 252000 non-null int64 12 Risk_Flag 252000 non-null int64 dtypes: int64(7), object(6) memory usage: 25.0+ MB

We see that half the features are numeric and half are strings, so they are probably categorical features.

Numerical data represents measurable quantities of a phenomenon. In data science, we call numerical data “quantitative data” because it describes the quantity of the object it represents.

Categorical data refers to the properties of a phenomenon that can be named. It involves describing the names or qualities of objects with words. In data science, categorical data is referred to as “qualitative data” since it describes the quality of the entity it represents.

Let us check if there are any missing values in the data.

data.isnull().sum()

Output:

Id 0 Income 0 Age 0 Experience 0 Married/Single 0 House_Ownership 0 Car_Ownership 0 Profession 0 CITY 0 STATE 0 CURRENT_JOB_YRS 0 CURRENT_HOUSE_YRS 0 Risk_Flag 0 dtype: int64

So, there is no missing or empty data here.

Let us check the data column names.

data.columns

Output:

Index(['Id', 'Income', 'Age', 'Experience', 'Married/Single',

'House_Ownership', 'Car_Ownership', 'Profession', 'CITY', 'STATE',

'CURRENT_JOB_YRS', 'CURRENT_HOUSE_YRS', 'Risk_Flag'],

dtype='object')

So, we get the names of the data features.

Analyzing Numerical Columns

First, we start with the analysis of numerical data.

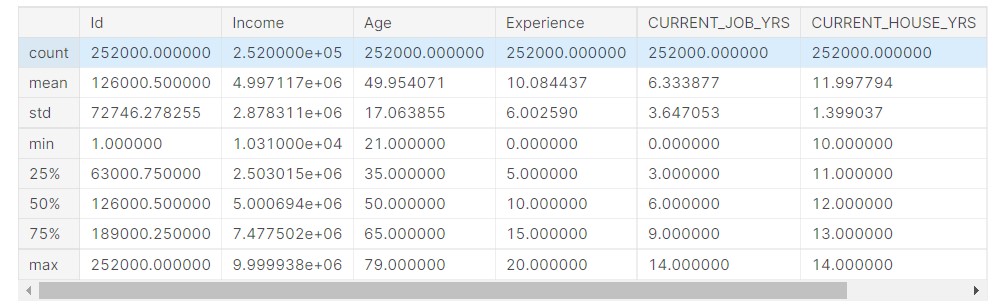

data.describe()

Output:

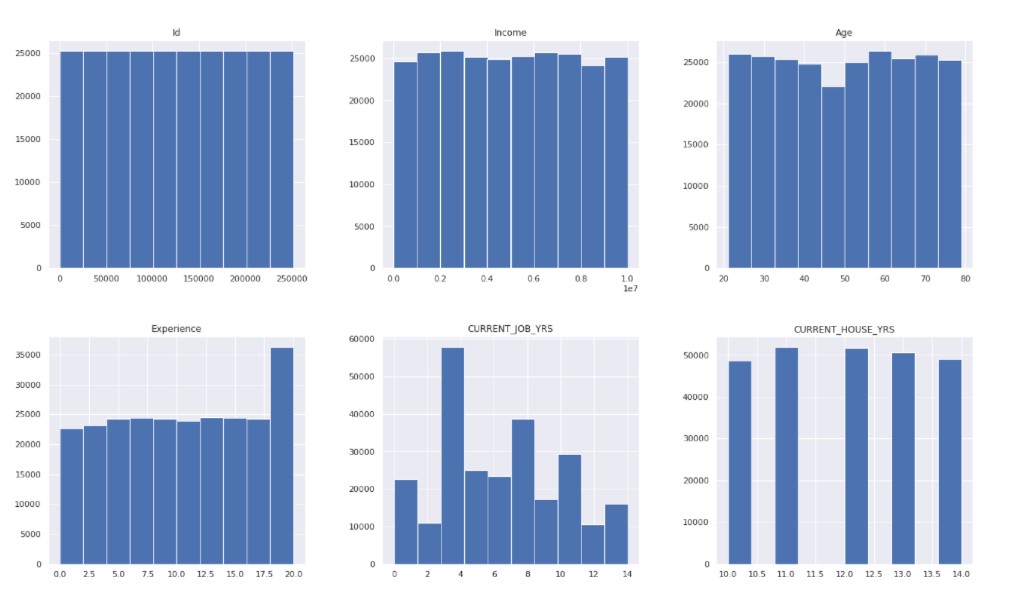

Now, we check the data distribution.

data.hist( figsize = (22, 20) ) plt.show()

Output:

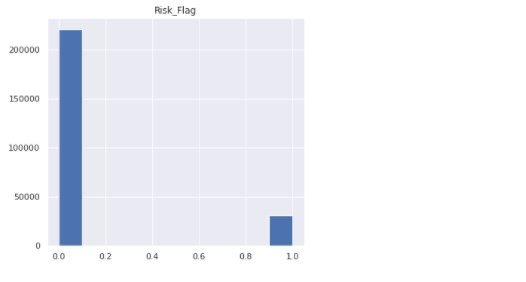

Now, we check the count of the target variable.

data["Risk_Flag"].value_counts()

Output:

0 221004 1 30996 Name: Risk_Flag, dtype: int64

Only a small part of the target variable comprises people who default on loans.

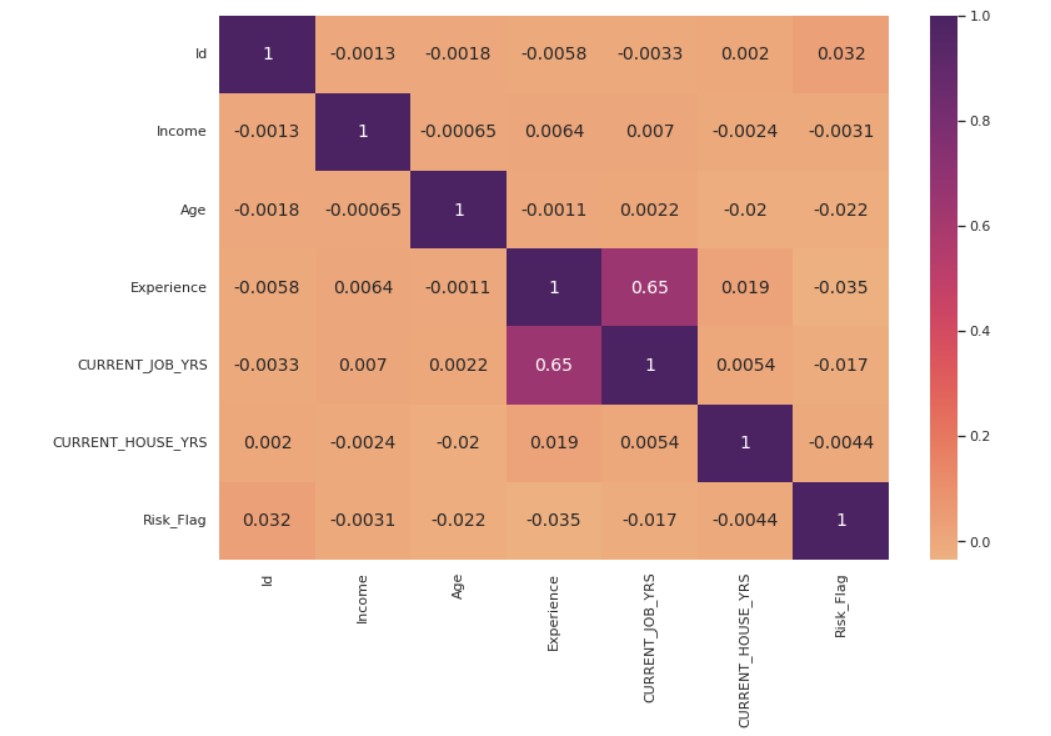

Now, we plot the correlation plot.

fig, ax = plt.subplots( figsize = (12,8) )

corr_matrix = data.corr()

corr_heatmap = sns.heatmap( corr_matrix, cmap = "flare", annot=True, ax=ax, annot_kws={"size": 14})

plt.show()

Output:

Analyzing Categorical Features

Now, we proceed with the analysis of categorical features.

First, we define a function to create the plots.

def categorical_valcount_hist(feature):

print(data[feature].value_counts())

fig, ax = plt.subplots( figsize = (6,6) )

sns.countplot(x=feature, ax=ax, data=data)

plt.show()

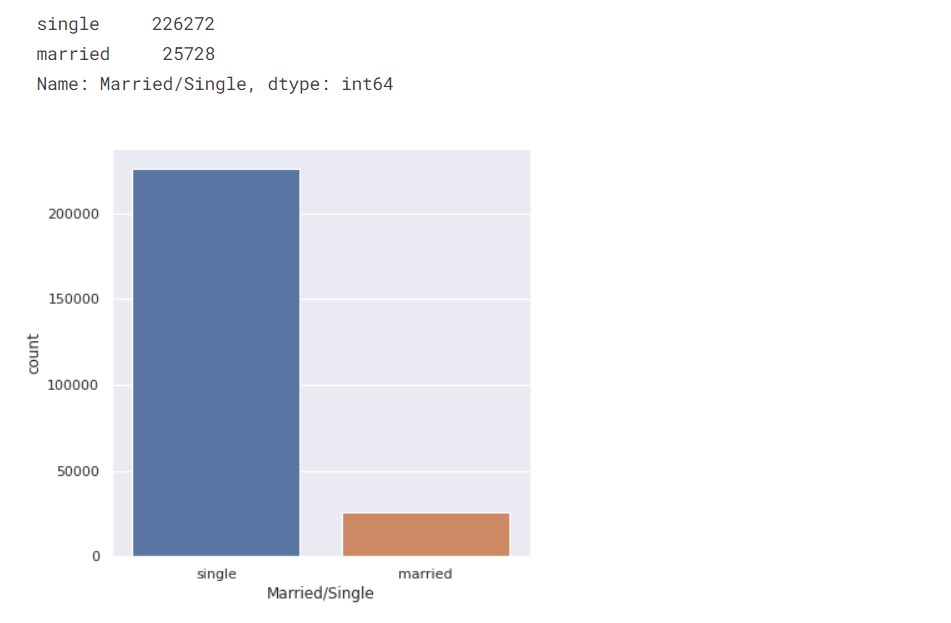

First, we check the count of married people vs single people.

categorical_valcount_hist("Married/Single")

Output:

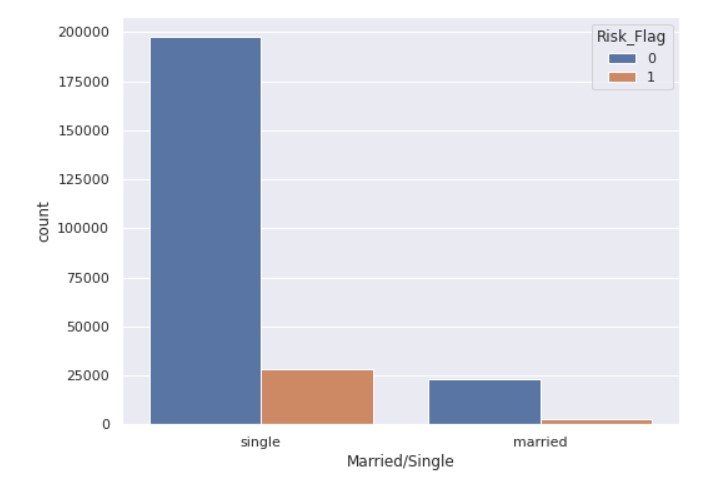

So, the majority of the people are single.

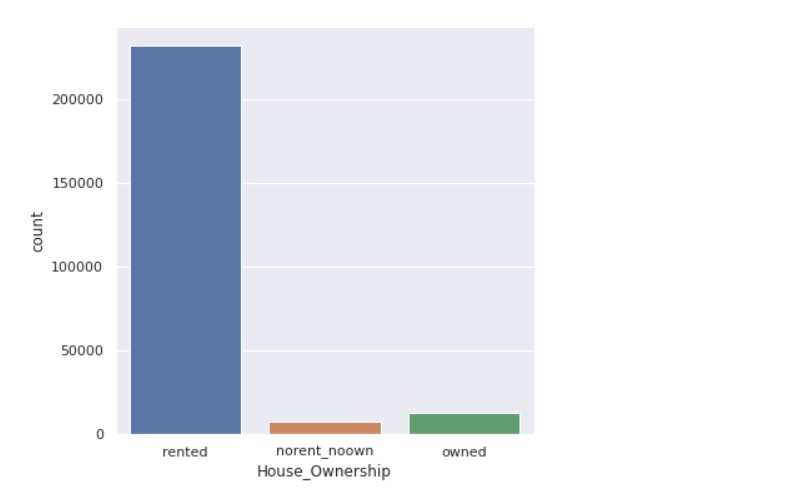

Now, we check the count of house ownership.

categorical_valcount_hist("House_Ownership")

Output:

Now, let us check the count of states.

print( "Total categories in STATE:", len( data["STATE"].unique() ) ) print() print( data["STATE"].value_counts() )

Output:

Total categories in STATE: 29 Uttar_Pradesh 28400 Maharashtra 25562 Andhra_Pradesh 25297 West_Bengal 23483 Bihar 19780 Tamil_Nadu 16537 Madhya_Pradesh 14122 Karnataka 11855 Gujarat 11408 Rajasthan 9174 Jharkhand 8965 Haryana 7890 Telangana 7524 Assam 7062 Kerala 5805 Delhi 5490 Punjab 4720 Odisha 4658 Chhattisgarh 3834 Uttarakhand 1874 Jammu_and_Kashmir 1780 Puducherry 1433 Mizoram 849 Manipur 849 Himachal_Pradesh 833 Tripura 809 Uttar_Pradesh[5] 743 Chandigarh 656 Sikkim 608 Name: STATE dtype: int64

Now, we check the count of professions.

print( "Total categories in Profession:", len( data["Profession"].unique() ) ) print() data["Profession"].value_counts()

Output:

Total categories in Profession: 51 Physician 5957 Statistician 5806 Web_designer 5397 Psychologist 5390 Computer_hardware_engineer 5372 Drafter 5359 Magistrate 5357 Fashion_Designer 5304 Air_traffic_controller 5281 Comedian 5259 Industrial_Engineer 5250 Mechanical_engineer 5217 Chemical_engineer 5205 Technical_writer 5195 Hotel_Manager 5178 Financial_Analyst 5167 Graphic_Designer 5166 Flight_attendant 5128 Biomedical_Engineer 5127 Secretary 5061 Software_Developer 5053 Petroleum_Engineer 5041 Police_officer 5035 Computer_operator 4990 Politician 4944 Microbiologist 4881 Technician 4864 Artist 4861 Lawyer 4818 Consultant 4808 Dentist 4782 Scientist 4781 Surgeon 4772 Aviator 4758 Technology_specialist 4737 Design_Engineer 4729 Surveyor 4714 Geologist 4672 Analyst 4668 Army_officer 4661 Architect 4657 Chef 4635 Librarian 4628 Civil_engineer 4616 Designer 4598 Economist 4573 Firefighter 4507 Chartered_Accountant 4493 Civil_servant 4413 Official 4087 Engineer 4048 Name: Profession dtype: int64

Data Analysis

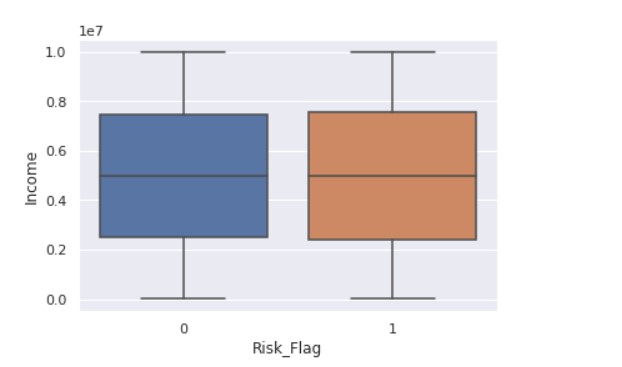

Now, we start with understanding the relationship between the different data features.

sns.boxplot(x ="Risk_Flag",y="Income" ,data = data)

Output:

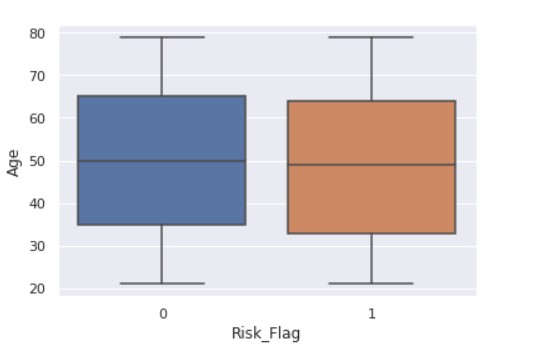

Now, we see the relationship between the flag variable and age.

sns.boxplot(x ="Risk_Flag",y="Age" ,data = data)

Output:

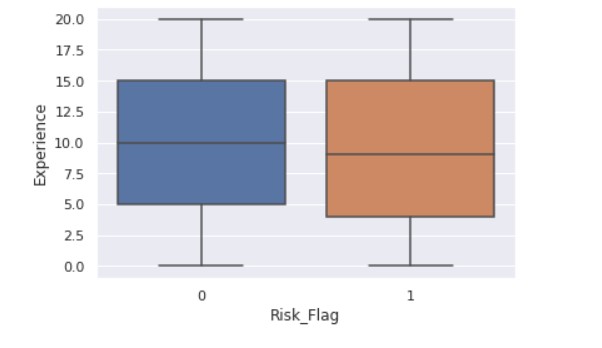

sns.boxplot(x ="Risk_Flag",y="Experience" ,data = data)

Output:

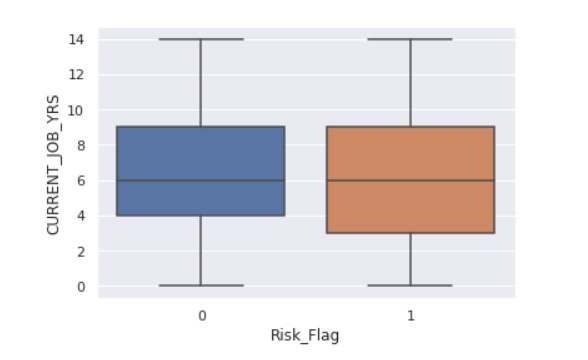

sns.boxplot(x ="Risk_Flag",y="CURRENT_JOB_YRS" ,data = data)

Output:

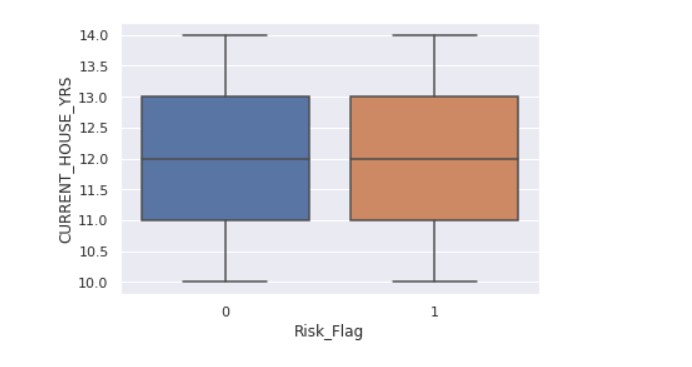

sns.boxplot(x ="Risk_Flag",y="CURRENT_HOUSE_YRS" ,data = data)

Output:

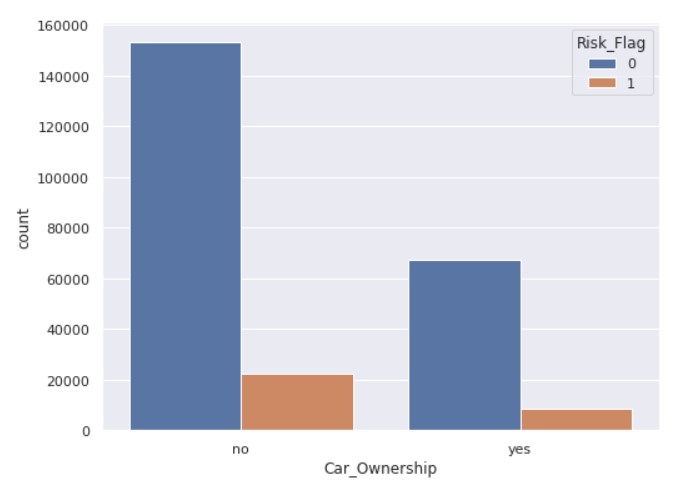

fig, ax = plt.subplots( figsize = (8,6) ) sns.countplot(x='Car_Ownership', hue='Risk_Flag', ax=ax, data=data)

Output:

fig, ax = plt.subplots( figsize = (8,6) ) sns.countplot( x='Married/Single', hue='Risk_Flag', data=data )

Output:

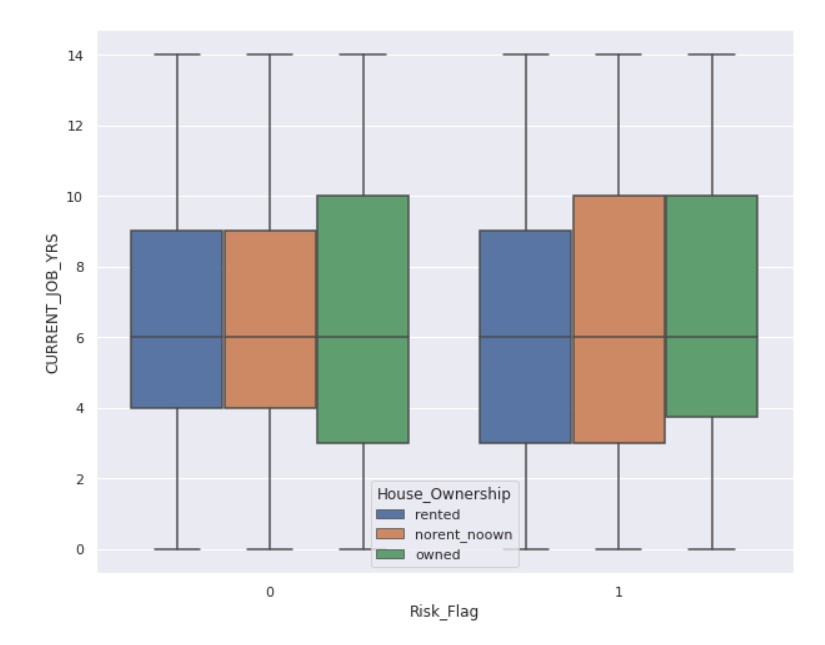

fig, ax = plt.subplots( figsize = (10,8) ) sns.boxplot(x = "Risk_Flag", y = "CURRENT_JOB_YRS", hue='House_Ownership', data = data)

Output:

Encoding

Data preparation is required in data science before moving on to modeling. In the data preparation process, we must complete many tasks. One of these critical responsibilities is the encoding of categorical data. We all know that most real-life data contains categorical string values, and most machine-learning models handle only integer values or other understandable formats. All models execute mathematical operations that various tools and methodologies can perform.

Encoding categorical data is turning categorical data into integer format so that data with transformed categorical values may be fed into models to increase prediction accuracy.

We will apply encoding to the categorical features.

from sklearn.preprocessing import LabelEncoder from sklearn.preprocessing import OneHotEncoder import category_encoders as ce

label_encoder = LabelEncoder() for col in ['Married/Single','Car_Ownership']: data[col] = label_encoder.fit_transform( data[col] )

onehot_encoder = OneHotEncoder(sparse = False) data['House_Ownership'] = onehot_encoder.fit_transform(data['House_Ownership'].values.reshape(-1, 1) )

high_card_features = ['Profession', 'CITY', 'STATE']

count_encoder = ce.CountEncoder()

# Transform the features, rename the columns with the _count suffix, and join to dataframe

count_encoded = count_encoder.fit_transform( data[high_card_features] )

data = data.join(count_encoded.add_suffix("_count"))

data= data.drop(labels=['Profession', 'CITY', 'STATE'], axis=1)

After the feature engineering part is complete, we shall split the data into training and testing sets.

Splitting the Data into Train and Test Splits

The train-test split measures the performance of machine learning models relevant to prediction-based Algorithms/Applications. This quick and simple approach allows us to compare our machine-learning model outcomes to machine results. By default, the Test set contains 30% of the real data, whereas the Training set contains 70% of the actual data.

We must divide a dataset into training and testing sets to assess how effectively our machine-learning model works. The train set is used to train the Machine Learning model, and its statistics are known. The second set is known as the test data set and is only used for predictions.

It is an important part of the ML chain.

x = data.drop("Risk_Flag", axis=1)

y = data["Risk_Flag"]

from sklearn.model_selection import train_test_split x_train, x_test, y_train, y_test = train_test_split(x, y, test_size = 0.2, stratify = y, random_state = 7)

We have taken the test size to be 20% of the data.

Random Forest Classifier

Tree-based algorithms like random forests are crucial in loan defaulter prediction and credit risk assessment. These algorithms are adept at handling classification and regression tasks, making them valuable in analyzing loan applications. Generating predictions based on training samples offers high accuracy and stability, which is crucial for identifying potential defaulters.

In the context of loan default prediction using machine learning, tree-based algorithms help minimize false negatives and positives, ensuring robust risk assessment. While individual decision trees may overfit training data, random forests mitigate this issue by averaging predictions from multiple trees, improving prediction accuracy.

In academic research, studies exploring the efficacy of tree-based algorithms in loan default prediction using machine learning can be found in reputable journals. Authors often provide DOIs for their work, facilitating citation and further research in this area. Additionally, comparisons between tree-based models and logistic regression models may offer insights into the strengths and limitations of each approach in credit risk assessment.

Now, we train the model and perform the predictions.

from sklearn.ensemble import RandomForestClassifier from imblearn.over_sampling import SMOTE from imblearn.pipeline import Pipeline

rf_clf = RandomForestClassifier(criterion='gini', bootstrap=True, random_state=100)

smote_sampler = SMOTE(random_state=9)

pipeline = Pipeline(steps = [['smote', smote_sampler],

['classifier', rf_clf]])

pipeline.fit(x_train, y_train)

y_pred = pipeline.predict(x_test)

Now, we check the accuracy scores.

from sklearn.metrics import confusion_matrix, precision_score, recall_score, f1_score, accuracy_score, roc_auc_score

print("-------------------------TEST SCORES-----------------------")

print(f"Recall: { round(recall_score(y_test, y_pred)*100, 4) }")

print(f"Precision: { round(precision_score(y_test, y_pred)*100, 4) }")

print(f"F1-Score: { round(f1_score(y_test, y_pred)*100, 4) }")

print(f"Accuracy score: { round(accuracy_score(y_test, y_pred)*100, 4) }")

print(f"AUC Score: { round(roc_auc_score(y_test, y_pred)*100, 4) }")

Output:

-------------------------TEST SCORES----------------------- Recall: 54.1378 Precision: 54.3306 F1-Score: 54.234 Accuracy score: 88.7619 AUC Score: 73.8778

The accuracy scores might not be up to par, but this is part of the overall process of predicting loan default.

Code: Here

Conclusion

Loan prediction using machine learning involves thorough exploratory data analysis (EDA) to understand dataset characteristics. Classification models are developed leveraging artificial intelligence algorithms, Utilizing Python libraries and techniques like boosting, random forest classifiers, and logistic regression. Evaluation metrics such as accuracy, precision, recall, F1-score, and AUC assess model performance in binary classification tasks. International conferences on data science and AI foster collaboration and innovation in risk assessment and management. This integrated approach enables effective loan default prediction, which is crucial for financial sector risk management.

Key Take Away

- The Random Forest approach is appropriate for classification and regression tasks on datasets with many entries and features likely to have missing values. It allows us to achieve a highly accurate result while avoiding overfitting.

- Furthermore, the random forest provides relative feature significance, enabling you to select the most important features. It is more interpretable than neural network models but less interpretable than decision trees.

- Encoding is necessary for categorical features so the ML algorithm can process them.

- Predicting loan default is highly dependent on demographics; people with lower incomes are more likely to default on loans.

We successfully performed the classification task using a Random Forest Classifier. I hope you liked my article on predicting loan default.

Frequently Asked Questions

Q1. Why is loan default prediction important?

A. Loan default prediction using machine learning is crucial for financial institutions to assess the risk of lending money to individuals or businesses. By accurately predicting the likelihood of default, lenders can make informed decisions regarding loan approval, interest rates, and loan terms, ultimately minimizing potential losses and maintaining a healthy loan portfolio.

Q2. What is the best model to predict loan default?

A. There isn’t a universally “best” model for predicting loan defaults, as it depends on various factors such as the nature of the dataset, the available features, and the lender’s specific requirements. However, commonly used models for loan defaulter prediction include logistic regression, decision trees, random forests, gradient-boosting machines, and neural networks.

Q3. What is the probability of default prediction?

A. Probability of default prediction refers to estimating the likelihood or probability that a borrower will fail to meet their loan obligations. This prediction is typically expressed as a numerical value ranging from 0 to 1, where 0 indicates low risk (unlikely to default) and 1 indicates high risk (likely to default). It is a quantitative measure for assessing credit risk and informing lending decisions.

Q4. What is the loan default prediction dataset?

The loan default prediction dataset typically consists of historical loan data, including various borrower attributes such as credit score, income, employment status, debt-to-income ratio, loan amount, loan term, and repayment history.

The media shown in this article is not owned by Analytics Vidhya and are used at the Author’s discretion.

Prateek is a dynamic professional with a strong foundation in Artificial Intelligence and Data Science, currently pursuing his PGP at Jio Institute. He holds a Bachelor's degree in Electrical Engineering and has hands-on experience as a System Engineer at TCS Digital, where he excelled in API management and data integration. Prateek also has a background in product marketing and analytics from his time with start-ups like AppleX and Milkie Way, Inc., where he was involved in growth campaigns and technical blog management. Recognized for his structured thinking and problem-solving abilities, he has received accolades like the Dr. Sudarshan Chakraborty Award for Best Student Performance. Fluent in multiple languages and passionate about technology, Prateek continues to expand his expertise in the rapidly evolving AI and tech landscape.