Introduction

Blockchain ecosystem has enabled us with a new way of perceiving, storing, and sharing data based on the concept of peer-to-peer technologies.

Blockchain gained popularity in the last decade for developing cryptocurrency exchanges, maintaining a foolproof medical history of patients, and immutable education records.

To get future-ready and develop an understanding of blockchain, it is fundamental to understand how a Blockchain transaction works and how new blocks are added to an existing blockchain.

What does a Blockchain ecosystem consist of?

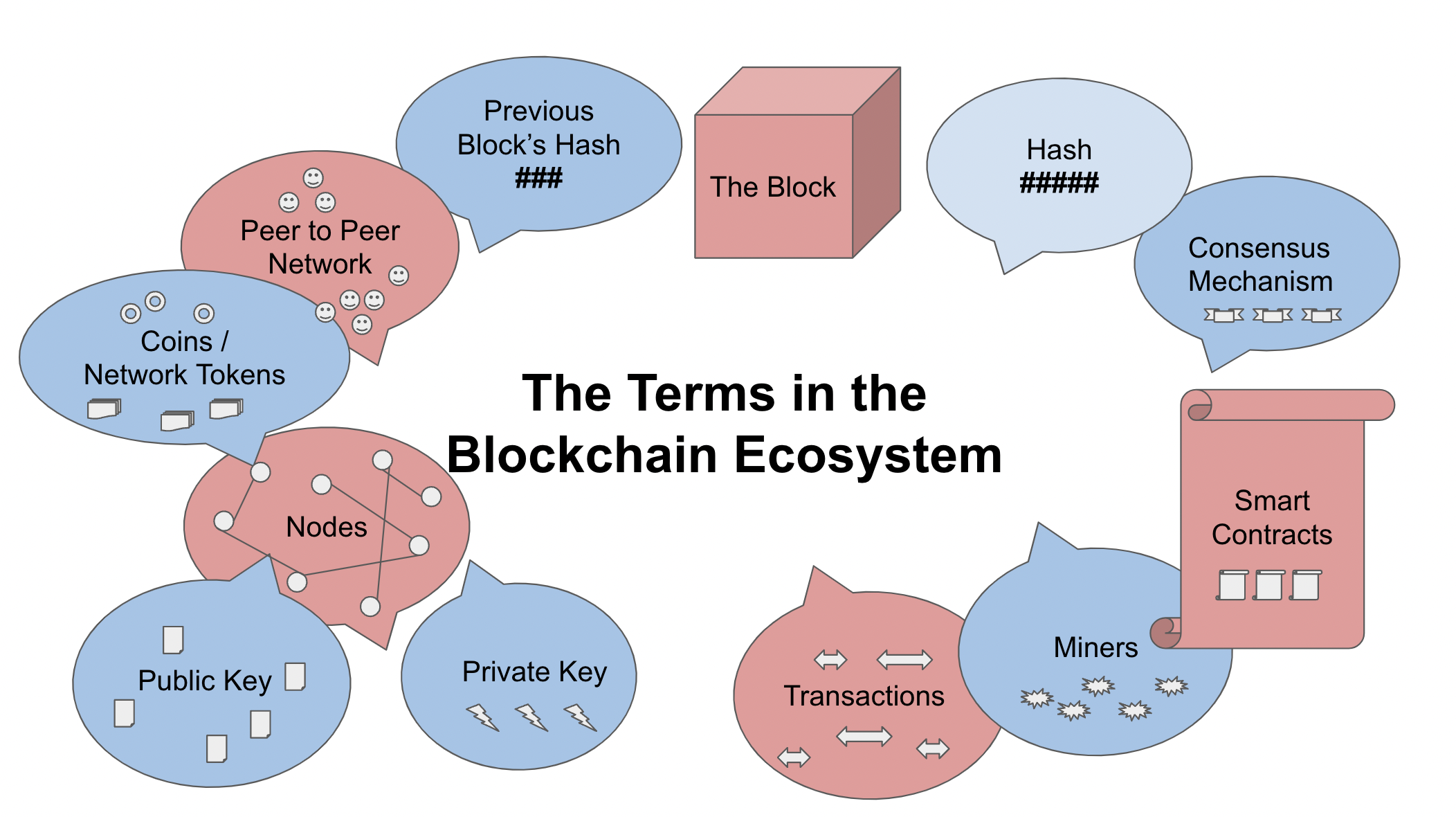

A blockchain ecosystem consists of the Blocks of Information, Hash, Previous block hash, Public key, Private key, Nodes(Compute Systems), and Peer to Peer networks at a high level.

-

Blocks – as mentioned earlier, are the basic data structures that form the Blockchain. Each Block holds information, is identified by a unique hash, and holds the hash address of the previous block.

-

Node – is an authorized user of the blockchain. A person with a computing machine can participate in the building and mining blocks in the blockchain network.

-

Hash – A unique key that identifies the Block.

-

Previous Block Hash – The hash address of the previous block to which the current block is connected.

-

Private key – a cryptographic version of identity – is a unique identifier of the candidate and can enable a person to perform a digital signature.

-

Public Key – a cryptographic key – which helps to identify a node in the blockchain network

-

Peer-to-Peer network – the group of nodes who are a part of the Blockchain.

-

-

Transactions – any interaction which involves an information exchange in terms of bitcoin investments, video content sharing, or medical record processing – is a blockchain transaction. A set of transactions form blocks containing information specific to a transaction. These represent the current state of a blockchain.

-

Miners – The nodes which participate in the validation of new Blocks or transactions.

-

Consensus Mechanism – the process by which the miners validate a block. For example, Proof of Work or Proof of Stake.

-

Network tokens – the cryptocurrencies, for example, bitcoins – can be used to incentivize blockchain transactions in monetary terms.

-

Smart contracts – can be thought of as a Piece of code – where all the rules are predefined to govern a transaction. And it is signed with the help of a private key. These are digital forms of legal contracts.

-

Cryptocurrency – is one of the use-cases built on Blockchain technology. Within a few lines of code, you can create a code that identifies a physical good, real estate, asset, or access rights.

How does a Blockchain transaction work?

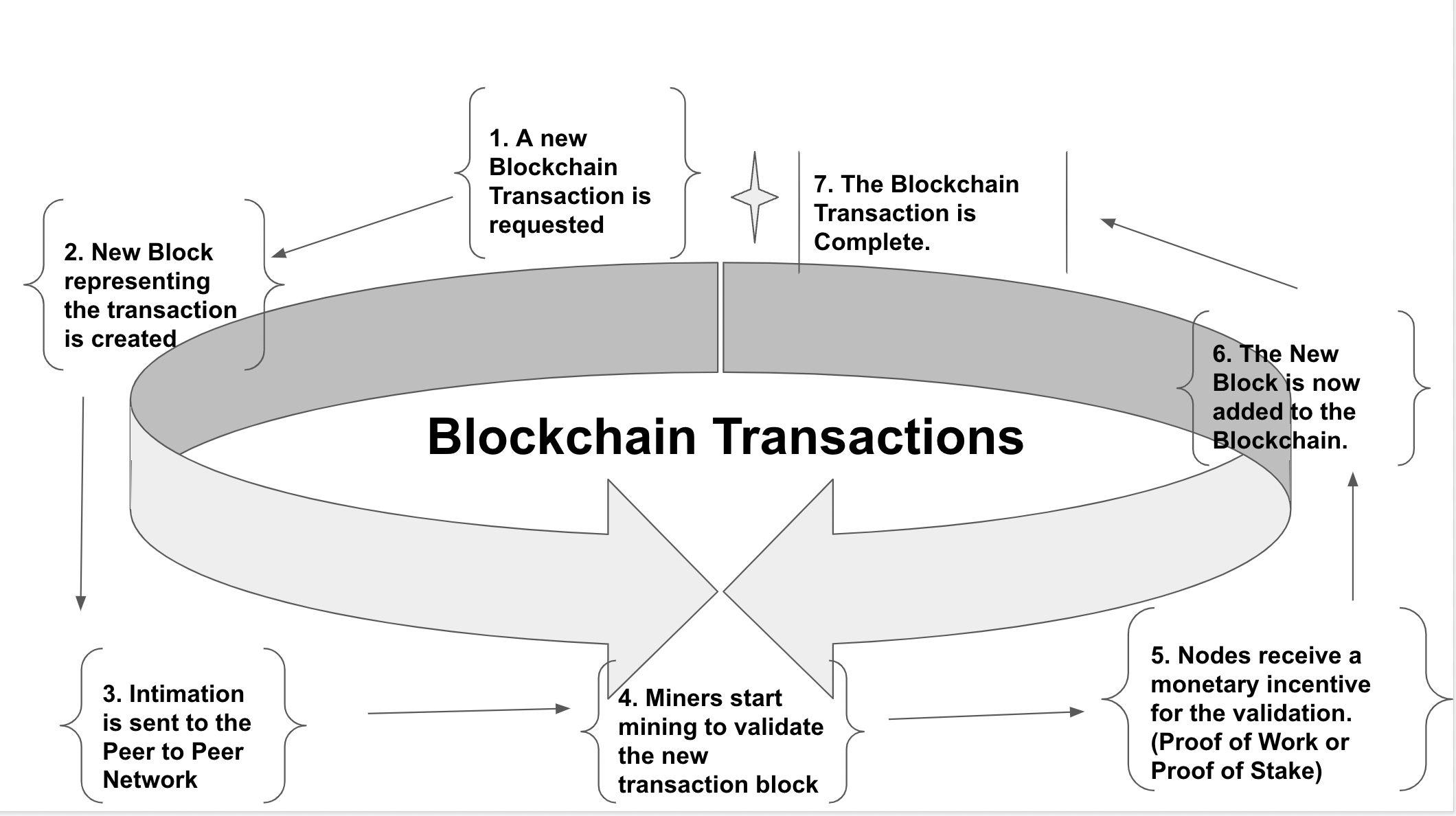

Any transaction that happens in the blockchain is monitored and recorded.

To understand the working of the Blockchain – let us understand with the example of Bitcoins.

The blockchain transactions work on the principle of consensus mechanism, rewards and penalty.

Any fair transaction on the blockchain is rewarded with monetary incentives like giving a set of bitcoins for that transaction. If a transaction is not accepted – a penalty has to be borne by the individual who tried to initiate that transaction. Or the penalty can also be in the form of not allowing the user to contribute to the blockchain in future instances.

To approve any transaction – Maximum voting is required. More than 51% of the people within the network must agree that the transaction is fair and are in favor of it.

To mine the blocks in a blockchain – ‘Proof of work is a concept that is widely adopted in the blockchain.

Proof of work – is a consensus mechanism that had been used in the early blockchain technology. Anyone in the network can participate in the mining of Bitcoins; the first one to recognize the Block gets the credit and monetary incentives in the form of Bitcoins which can further be introduced into the Value-chain. It is a Reliable, Fair, Real-time, and transparent system to ensure that the blockchain’s participants have contributed to the network.

Proof of Stake – is another consensus mechanism – which has been introduced in recent blockchains. This encourages participation in the Blockchain development in mining – with stakes. Anyone who wants to participate in the Blockchain development will have to come in with a commitment in the form of bitcoins or any other incentive – finally – a node that wins the stake will contribute to the piece of work. How is the worthy stakeholder selected – this is based on the models which account for the quantum of the amount put at stake, history of participation in the blockchain, and randomness to ensure fairness.

What was the need to invent Blockchain?

Every time we use the internet or download new applications on our Android or iOS phones – we give access to many personal data points to the entities who have created the application. Blockchain technology was invented to promote an internet ecosystem – where the users hold more power over their data and right to privacy.

Blockchain enables a more secure and democratized way of dealing with data – where the data ownership remains with the users rather than the Giant conglomerates. Also, the time, energy, and right to information monetization remain with the User.

It can help create a foolproof tracking system for Medical Records of a patient, the Education history of Students, and Fair and transparent trading in the Cryptocurrency markets.

What are the advantages of Blockchain?

The core premise of the Blockchain invention was to ensure decentralized distributed systems.

-

Transparent – accessible to all

-

Fair – not governed by a central authority

-

Immutable – once a block is created – it cannot be changed, and every transaction is recorded in the history of time.

What are the disadvantages of Blockchain technology?

High compute power – Negative impact on the environment :

Blockchain development requires machines with very high computing efficiency. A blockchain is only effective if it has a powerful peer-to-peer network. The more nodes in the network – the higher the computation costs and power required. This makes blockchain a very high carbon footprint technology.

Less scalable :

Since the blockchain requires very high computational power, knowledge about new technologies, and specific subject matter expertise, it is tough to scale and time to grow.

If – you can hack 51% of the network – the entire blockchain can be hacked. While this is difficult to achieve – but there is a possibility.

What is Mining in Blockchain? Why is it required?

Mining can be understood as looking for the source of origin of a Blockchain transaction.

Mining is most commonly associated with minerals and ores in the physical world.

To get metals – we first identify the Ores of the metals and then start the mining process – to collect the ores from the depths of the earth and then extract the metal from the raw form of ores.

Similarly, in a Blockchain ecosystem, we mine the Blocks to get information about 2 things:-

-

To detect the changes made in the already existing blocks of the blockchain.

-

To validate any new blocks which are added to the blockchain

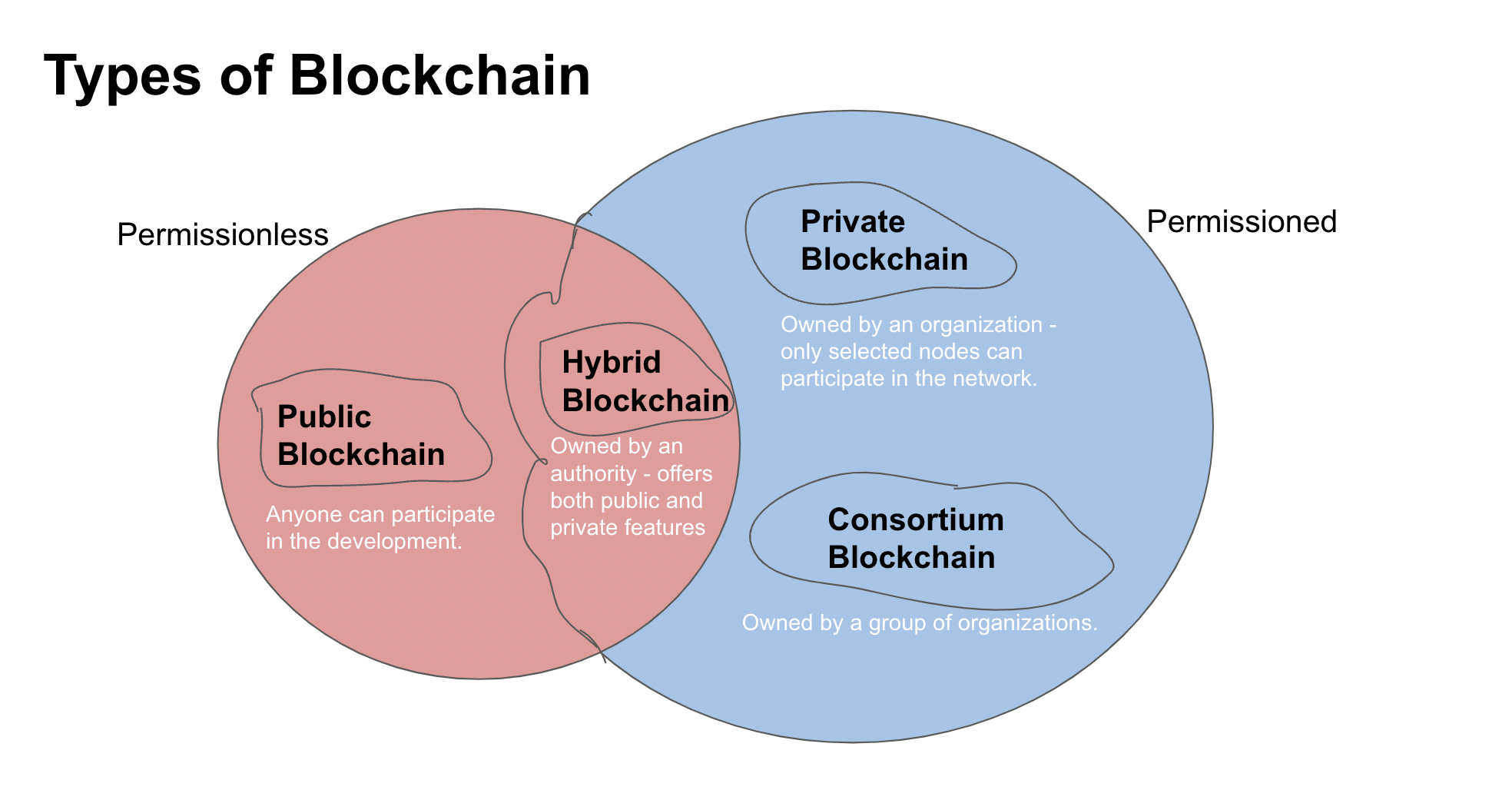

What are the different types of Blockchain?

The basic need of the blockchain ecosystem is to store the data and make the transactions more democratic and transparent.

We can understand this with the example of public and private Internet domains.

Public BlockChain

The public blockchain can be considered an open source software like Python – where anyone can come and contribute to the development of the Blockchain. The information to be added to the Blockchain and any support required to develop the blockchain is open to the entire network.

Private BlockChain

- Private blockchain – can be understood with an example of a closed network domain – for example, the Domain network of a school – which is accessible only to the school staff, teachers, students, and parents.

- Similarly, only the people who belong to a private blockchain network can participate in the development and transactions within the private blockchain. An organization owns it.

- The decentralized network is formed within the private network – i.e., the participants’ select pool.

Hybrid BlockChain

- A blockchain under the ownership of an organization that offers both Public and Private features is a Hybrid Blockchain.

- Permissionless features are enabled to develop some portion of the Blockchain.

Consortium BlockChain

- A blockchain owned by a major group or group of organizations is known as a consortium blockchain. It is under regulation.

- A Consortium Blockchain can have both public and private features.

How is my data secure on Blockchain?

It is a persistent question in the users’ minds – that if the data is democratized – and freely accessible to all – present on the entire blockchain network – how is my data secure?

This can be understood with the help of a Monthly bank statement which is password protected.

Even if the file is on multiple laptops or machines, the information inside it can only be seen by individuals with present passwords.

In a Peer to peer network – all computers in the network have the same level of information

A peer-to-peer network ensures transparent access to information, but the information can only be accessed by individuals who have permission.

Are the transactions that take place on Blockchain fair?

Now the question arises if the Blockchain is not under the control of any central authority – how do we ensure that the transactions happen fairly?

The answer lies in two aspects:-

-

The Economic incentives – are associated with each transaction.

-

The Maximum Voting – principle by the peer group.

Any Blockchain at the beginning – assumes that all parties involved in the beginning are corrupt. You can imagine – that the blockchain node is like a Nephron. How does a nephron transfer information – from one to another – using synapse?

A Network – actor in a blockchain – is similar to a synapse in the Nephron – which gets activated when the need arises to make a transaction within a blockchain.

Network – actors do not trust each other in the beginning. How do we make sure that they trust each other – this job is done via network tokens – like bitcoin.

In blockchain – no one is bound legally to another party through a contract.

It is an architecture – which incentivizes network actors which operate through a centralized governing protocol – rather than a regulatory body.

Every new transaction occurs, the network actors do a service to the blockchain network by ensuring the transaction happens instead of the predefined rules. For that, they earn bitcoin (or the network tokens).

Conclusion

Blockchain transactions utilize a unique consensus, validation, and fairness mechanism to get executed. Once done – the transactions are recorded in the history of time and are immutable.

The strength of the peer-to-peer network, along with the choice of the consensus mechanism, lies at the heart of blockchain transactions and development.

Blockchain Distributed Ledger technology is here to stay. It is the backbone of the next-gen of the internet on which Web 3.0 is built. But since the skill sets and pre-requisites required to adopt blockchain are very niche and resource intensive, the market adoption is slower.

Can you think of more advantages and disadvantages of the Blockchain ecosystem?

Please mention it in the comments section below.